It Is Not About the Model

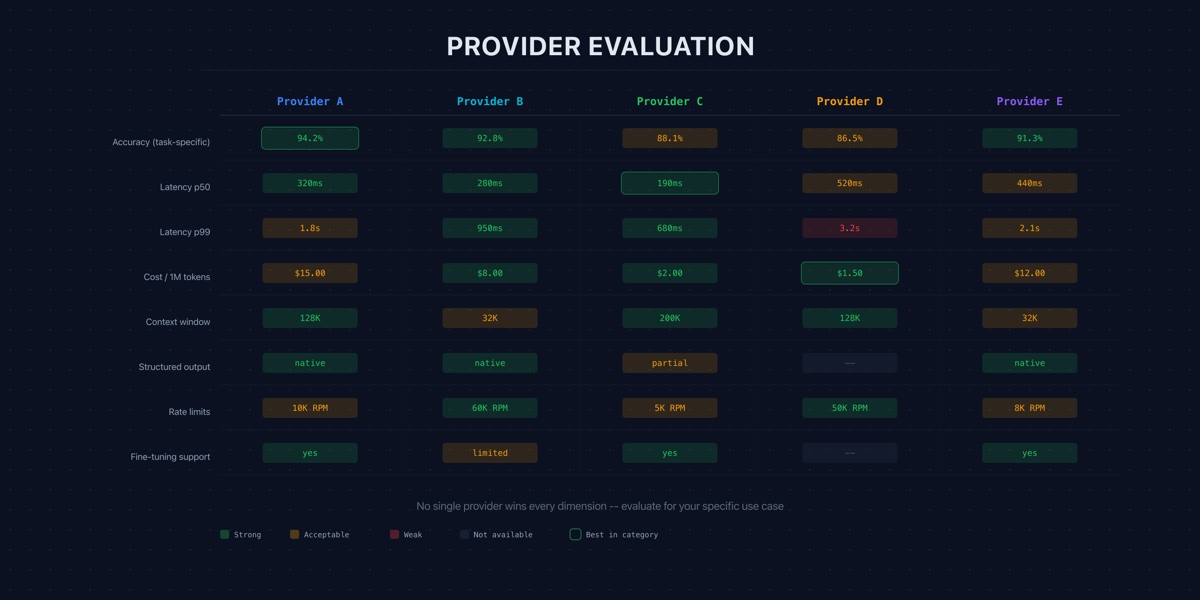

Most teams start their LLM provider evaluation with a benchmark comparison. Which model leads the Chatbot Arena? Which one generates the best code?

This is the wrong starting point. Model quality is the most visible dimension of provider selection and the least durable. Benchmark leaders change quarterly. The model that tops the leaderboard when you sign the contract may be third by the time your integration ships. And quality differences between frontier models on production tasks — classification, extraction, summarization — are often smaller than the gap between a well-engineered prompt and a poor one.

The decisions that determine total cost, operational risk, and ability to change course are the ones procurement teams evaluate last: pricing, data handling, SLAs, migration costs, and multi-provider strategy. These are vendor decisions, not model decisions.

The Pricing Landscape

The price of LLM inference varies by three orders of magnitude. GPT-5.2 costs $1.75/$14.00 per million tokens (input/output). Claude Sonnet runs $3.00/$15.00. Gemini Flash costs $0.10/$0.40 [S1]. That is a 1,000x gap between the cheapest and most expensive options for services that are, in many production contexts, functionally interchangeable.

The spread matters because most workloads are not homogeneous. A customer support system might need frontier reasoning for 10% of queries — escalation decisions, complex policy interpretation — and commodity classification for the other 90%. Routing everything through a $15.00-per-million-output-token model because the hardest queries require it is the most common and most expensive mistake in LLM cost management.

Model routing — classifying requests by complexity and directing simple queries to cheap models — is the single highest-leverage cost optimization available. Teams that implement even basic routing typically reduce inference costs by 60-80% without meaningful quality degradation on the bulk of traffic.

Pricing also shifts rapidly. Contracts with long lock-in periods and fixed per-token rates expose you to paying above-market rates as the industry price curve falls. Favor usage-based terms with renegotiation windows.

Data Handling Differences

For regulated industries, data handling is often the gating factor for provider selection.

The major providers have converged on a baseline: all commit to not training on enterprise API data by default [S2]. But the baseline obscures meaningful differences. Security certifications differ significantly — Anthropic holds ISO 42001, specific to AI management systems, while Google achieved FedRAMP High authorization first among AI providers [S2]. The certification that matters depends on your regulatory context: healthcare, financial services, defense, and government each have different requirements.

Beyond certifications, operational details matter. How long are request logs retained? Where is inference physically executed? Can you specify the jurisdiction? These questions do not have uniform answers across providers and may not be publicly documented. They must be negotiated as part of an enterprise agreement.

For organizations subject to GDPR, HIPAA, or sector-specific data residency requirements, the provider’s data handling posture can narrow the field before you evaluate a single benchmark.

The SLA Gap

Neither OpenAI nor Anthropic publish public SLAs for uptime or latency [S3]. There are no publicly available contractual commitments for API availability, response time percentiles, or error rate ceilings from the two largest LLM API providers.

This is unusual for infrastructure that teams build production systems on. Cloud providers publish detailed SLAs with financial remedies. Database vendors do the same. LLM API providers, despite sitting in the critical path of production applications, operate without comparable commitments.

Enterprises that require SLAs must negotiate custom terms as part of enterprise agreements [S3]. Do this before committing to a provider, not after. The absence of a public SLA does not mean the provider will not offer one — it means you must ask explicitly, and the terms will reflect your negotiating position.

Design for provider failure regardless of SLA terms. An SLA is a financial remedy, not a guarantee. If your product cannot tolerate an hour of downtime, you need a failover strategy, not just a credit clause.

Hidden Costs: Migration and Lock-In

The most underestimated cost in provider selection is switching.

Survey data puts the average LLM migration at $315,000 — roughly twice the initial integration investment [S4]. This includes prompt rewriting, evaluation pipeline reconstruction, output format adaptation, and operational disruption [S4].

Migration cost creates lock-in, and lock-in undermines negotiating leverage. A team that cannot credibly threaten to switch will pay more over time — not because the provider is malicious, but because vendor relationships favor the party with more options.

The antidote is building provider-agnostic from the start. An abstraction layer that normalizes API calls, prompt formats, and output parsing across providers does not eliminate migration cost — prompts still need retuning — but it reduces structural switching cost and converts migration from a multi-quarter project to a multi-week one.

Multi-Model Strategy

The market is already moving in this direction. Thirty-seven percent of enterprises deploy five or more models in production [S5]. This is deliberate strategy, not experimentation.

Multi-model deployment enables four capabilities a single-provider commitment does not:

Cost optimization through routing. The 1,000x pricing gap [S1] makes task-based routing the most impactful cost lever available.

Risk diversification. If one provider experiences an outage, traffic fails over to another. The cost of maintaining multiple active integrations is small relative to production downtime.

Continuous benchmarking. With active integrations, you evaluate new models against your tasks and shift traffic when better options emerge. Provider selection becomes ongoing optimization, not a one-time decision.

Negotiating leverage. A team that demonstrably runs on multiple providers has credible alternatives — the strongest position for negotiating pricing and SLAs.

The average reported ROI for LLM infrastructure investment is $3.70 per dollar spent [S5]. Multi-model strategies protect that ROI by ensuring you never overpay for any given task and never depend on a single provider’s availability.

A Decision Framework

Provider evaluation should proceed in this order — not because model quality does not matter, but because the other dimensions are harder to change after the fact.

1. Data governance fit. Does the provider’s data handling, certification portfolio, and geographic infrastructure meet your regulatory requirements? This is a binary filter.

2. SLA availability. Will the provider commit to contractual uptime and latency guarantees? Negotiate before signing.

3. Total cost of ownership. Per-token pricing at projected volume, plus routing infrastructure, plus ongoing prompt maintenance and evaluation. A provider 2x cheaper per token but requiring 3x more tokens is not cheaper.

4. Migration cost and lock-in risk. How tightly does your integration couple to this provider’s API format and model behavior? Factor the $315K average migration cost [S4] into TCO, amortized over the expected relationship duration.

5. Model quality on your tasks. Evaluate on your actual production tasks with your actual prompts — not public benchmarks.

This ordering is deliberate. Data governance and SLAs are constraints that narrow the field. TCO and lock-in are structural costs that compound. Model quality is what you optimize within the feasible set.

What This Means for Your Team

Lead with constraints, not benchmarks. Determine what data can leave your infrastructure, what uptime you require, what your 12-month spend looks like. Build provider-agnostic from day one. Negotiate SLAs before you sign.